AI Data Center Power Consumption in 2026: The Complete Numbers

The Brief

The Pulse Data centers consumed roughly 415 terawatt-hours of electricity in 2024, about 1.5% of the world’s total, and the International Energy Agency projects that figure will more than double to around 945 TWh by 2030, slightly more than Japan’s entire annual electricity consumption today. AI is the reason: electricity use by AI-focused data centers […]

Why It Matters

The story matters because it changes how buyers, builders, or policymakers should read the AI Infrastructure market.

Watch Next

Watch whether the signal becomes a budget, procurement, or platform decision in the next cycle.

The Pulse

Data centers consumed roughly 415 terawatt-hours of electricity in 2024, about 1.5% of the world’s total, and the International Energy Agency projects that figure will more than double to around 945 TWh by 2030, slightly more than Japan’s entire annual electricity consumption today. AI is the reason: electricity use by AI-focused data centers grew about 50% in 2025 alone, and the IEA’s satellite tracking shows dedicated AI facilities more than tripled in capacity over 18 months. The constraint on AI is no longer chips. It is megawatts. This page tracks the numbers that matter: consumption today, demand per facility, power density per rack, every nuclear deal signed by a hyperscaler, and what US utilities are actually filing with regulators.

How much power do AI data centers use in 2026?

The short answer: global data centers drew approximately 415 TWh in 2024, and demand grew another 17% in 2025, in line with the IEA’s projections. The US accounts for the largest share at roughly 45%, followed by China at 25% and Europe at 15%.

The honest answer is that nobody can isolate AI’s share precisely, because most facilities run mixed workloads. The credible estimates disagree, and that disagreement is worth showing rather than hiding.

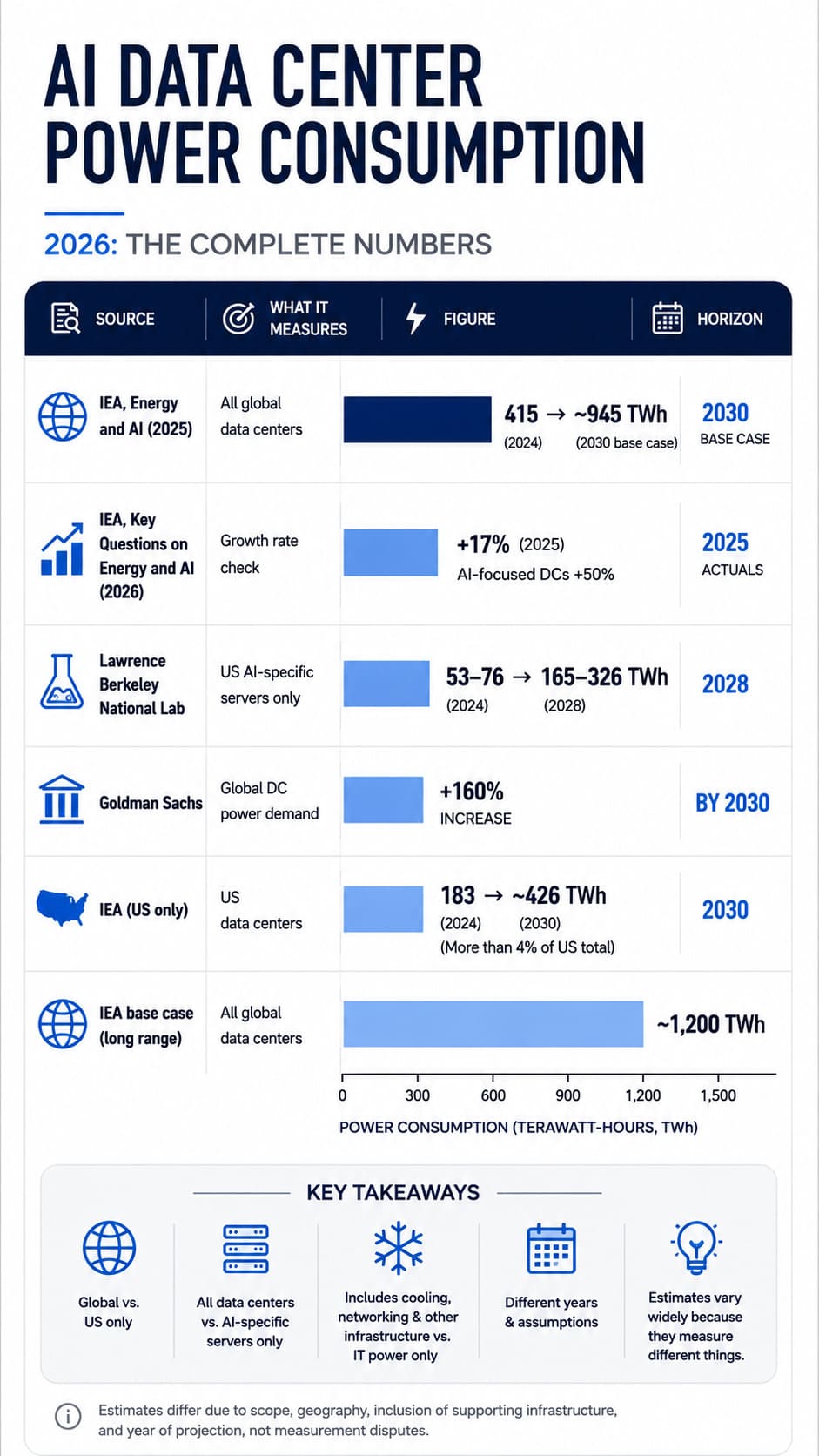

Table 1: How the major estimates compare

| Source | What it measures | Figure | Horizon |

| IEA, Energy and AI (2025) | All global data centers | 415 TWh (2024) to ~945 TWh | 2030 base case |

| IEA, Key Questions on Energy and AI (2026) | Growth rate check | +17% global DC demand in 2025; AI-focused DCs +50% | 2025 actuals |

| Lawrence Berkeley National Lab | US AI-specific servers only | 53-76 TWh (2024) to 165-326 TWh | 2028 |

| Goldman Sachs | Global DC power demand | +160% increase | By 2030 |

| IEA (US only) | US data centers | 183 TWh (2024, more than 4% of US total) to ~426 TWh | 2030 |

| IEA base case (long range) | All global data centers | ~1,200 TWh | 2035 |

Why the LBNL number looks so much smaller than the IEA number: it counts only AI-specific server consumption inside US facilities, not cooling, networking, conventional servers, or the rest of the world. When you see wildly different AI power consumption figures quoted in headlines, the discrepancy is almost always a scope difference, not a measurement dispute.[IEA — Energy and AI 2025]

Two more context numbers worth keeping in mind. The US, by 2030, is projected to use more electricity for data centers than for producing aluminium, steel, cement, and chemicals combined. And the capital is already committed: the largest technology companies spent over $400 billion in capex in 2025, with 2026 spending expected to rise roughly another 75%, more than global investment in oil and gas production.[IEA — Key Questions on Energy and AI 2026]

The concentration matters as much as the total. Nearly half of US data center capacity sits in just five regional clusters. Data centers consume around 26% of Virginia’s electricity and roughly 21% of Ireland’s. The grid problem is local before it is national.

How many megawatts does a single AI data center use?

There are now four distinct size classes, and the gap between them is enormous.

Table 2: AI facility size classes in 2026

| Class | Typical IT load | Example | Status |

| Enterprise / colocation | 5-25 MW | Standard colo facility | Legacy baseline |

| Hyperscale campus (pre-AI era) | 30-50 MW | Typical 2015-era hyperscale build | Superseded |

| AI hyperscale campus | 200-500 MW | Current baseline for new builds | Operating / under construction |

| Frontier training cluster | 1 GW+ | Stargate Abilene, xAI Colossus 2, Meta Prometheus | Coming online 2026-2027 |

A typical AI-focused hyperscale facility consumes as much electricity annually as about 100,000 households, per the IEA, and the largest ones under construction are expected to draw roughly 20 times that. The gigawatt class becomes real in 2026.

Table 3: Gigawatt-class AI facilities: Named projects

| Project | Operator | Power scale | Location | Timeline |

| Stargate (Abilene + 5 new sites) | OpenAI / Oracle / SoftBank | ~7 GW planned, targeting 10 GW / $500B program | Texas + multiple US states | Abilene scaling through 2026 |

| Colossus 2 | xAI | 550,000+ GPUs, targeting beyond 1 GW | Memphis, Tennessee | Scaling through 2026 |

| Prometheus | Meta | ~1 GW supercluster | Ohio | 2026 |

| Hyperion | Meta | Up to 5 GW across 11 buildings (~500 MW each) | Louisiana | Multi-year buildout |

| New Carlisle campus | Anthropic / Amazon | ~1 GW class | Indiana | 2026 |

| Fairwater / Fayetteville | Microsoft | Approaching 1 GW; Fairwater projected to exceed $100B total cost | Wisconsin / North Carolina | 2026 onward |

For scale: a 1 GW facility requires roughly the output of a single large nuclear reactor (a Westinghouse AP1000 is rated around 1.1 GW). We are building warehouses that need their own power plants.[Data Center Frontier — Stargate expansion]

AI data center power density: kW per rack, explained

Power density is the metric that explains why old data centers cannot simply be retrofitted for AI.

Table 4: Rack power density by generation

| Generation | Power per rack | Cooling |

| Legacy CPU rack | 5-15 kW | Air |

| Early AI / GPU era (A100) | 20-40 kW | Air, at its limit |

| H100 era | ~40 kW | Air-cooled infrastructure breaks here |

| Nvidia GB200/GB300 NVL72 | 120-140 kW | Direct liquid cooling, mandatory |

| Rubin-class (2027 roadmap) | 250-900 kW projected | Liquid; 800 VDC architectures in development |

| OCP 1 MW rack designs | ~1,000 kW | Next-generation power distribution |

A GB200 NVL72 rack packs 72 GPUs operating as one logical unit and is provisioned with roughly 264 kW of power shelf capacity to feed compute and NVLink networking. Direct liquid cooling on these systems captures about 98% of heat output, which is why liquid cooling went from exotic to mandatory in roughly two years.

The planning gap is the real story. Industry surveys put the average hyperscaler facility design assumption around 36 kW per rack, projected to reach 50 kW by 2027. The hardware actually shipping today draws 120 kW or more. That 2-3x gap between what facilities were designed for and what the silicon demands is why so much existing capacity is functionally obsolete for frontier AI, and why new builds dominate the pipeline.

Training vs inference: Where the power actually goes

The popular image of AI power consumption is a giant training run. The data says otherwise: an estimated 80-90% of AI computing is now spent on inference, the everyday serving of queries, not training.

This distinction matters enormously for grid planners. Training is spiky and schedulable; in principle, a training cluster can ramp down during a grid emergency. Inference is customer-facing, latency-sensitive, and runs around the clock, which is why utilities treat AI data centers as extremely high load-factor customers. Dominion reported its large data center customers operating at an 82% load factor in 2024, and Duke plans around 80% for new large loads. For comparison, that is the consumption profile of an aluminium smelter, except smelters do not double in number every couple of years.

The newer demand drivers compound this: video generation, reasoning models, and agentic workloads all consume materially more energy per task than simple text queries. The IEA notes that even as efficiency per query improves, application growth is outrunning it.

The nuclear answer: Every hyperscaler nuclear deal, tracked

In under two years, big tech signed contracts representing roughly 10 GW of current and future nuclear capacity in the US. This table is updated monthly.

Table 5: Hyperscaler nuclear deals as of June 2026

| Buyer | Counterparty / plant | Capacity | Structure | Power flows |

| Microsoft | Constellation, Three Mile Island Unit 1 restart (renamed Crane Clean Energy Center) | 835 MW | 20-year PPA; ~$1.6B restart cost; DOE LPO ~$1.5B loan guarantee closed Nov 2025 | Expected 2027-2028 |

| Amazon | Talen Energy, Susquehanna (PA) | Up to 1.92 GW | 17-year PPA; ~$20B AI campus investment at the site | Phased, underway |

| Amazon | X-energy | Up to 12 Xe-100 SMRs (~960 MW potential) | ~$700M investment | Early 2030s |

| Meta | Constellation, Clinton plant (IL) | 1.1 GW | 20-year PPA | From June 2027 |

| Meta | TerraPower, Oklo, Vistra (portfolio) | Up to ~6.6 GW combined commitments including RFP for 1-4 GW new nuclear | PPAs + development agreements | Late 2020s-2030s |

| Kairos Power | Up to 500 MW SMR fleet (first US corporate SMR fleet deal) | Development agreement | Early 2030s | |

| NextEra, Duane Arnold (IA) restart | ~600 MW | PPA | From ~2029 |

Read the structure of these deals, not just the megawatts. Twenty-year PPAs at reported premiums to wholesale rates are hyperscalers telling capital markets they expect AI electricity demand to persist for decades. The Three Mile Island restart is the symbolic centrepiece: the site of America’s most famous nuclear accident in 1979, brought back specifically to feed Microsoft’s AI workloads.[AI Business — Meta nuclear deals hyperscaler tracker]

The uncomfortable timing problem: none of this nuclear capacity arrives fast enough. The first restart electrons land in 2027-2028; SMRs arrive in the 2030s. AI demand is compounding now. The near-term gap is being filled overwhelmingly by natural gas, which is the part of this story that sustainability press releases tend to skip.

Are US utilities really citing AI demand in their filings? Yes. Here is the paper trail.

Press releases can exaggerate. Regulatory filings carry legal weight, and the filings are unambiguous.

The aggregate picture first: Grid Strategies’ national load growth analysis found that five-year US peak demand forecasts grew six-fold in just four years, with roughly 90 GW of the 166 GW in forecast peak load growth tied to data centers.

Georgia Power

Its 2025 Integrated Resource Plan, approved by the Georgia Public Service Commission, plans for roughly 8,500 MW of load growth by 2030, driven primarily by data centers. In December 2025, the GPSC certified close to 10 GW of new capacity, over staff warnings that much of the forecast rested on a pipeline of prospective customers rather than executed contracts, an over-forecasting risk that could leave ratepayers holding stranded assets if the demand never materialises. [Perkins Coie — Georgia PSC generation expansion analysis]

Dominion Energy (Virginia)

Dominion has proposed a dedicated rate class for customers of 25 MW or more with high load factors, built around 14-year take-or-pay style commitments designed to protect other ratepayers from stranded costs. Its five-year capital plan rose to about $50 billion, with data centers cited as a primary driver.

Duke Energy (Carolinas)

Duke raised its five-year capex plan to roughly $83 billion, a double-digit increase, and plans around 5 GW of new natural gas capacity by 2029 to serve data center and industrial growth. Notably, a Duke-commissioned study published in February 2026 found that flexible data center loads could avoid tens of billions in new plant costs nationally, an early signal that curtailable AI load may become a regulatory bargaining chip.

The ratepayer question

US utilities collectively plan on the order of $1 trillion-plus in spending through 2030, and consumer advocates estimate hundreds of billions of that could flow through to residential bills. The EIA projects average US residential electricity prices rising about 5% in 2026. Expect ‘who pays for AI’s grid’ to become a state-level political fight in the 2026 election cycle; it has already started in Georgia, Virginia, and Ohio rate cases.

AI electricity demand by 2030: the projections, compared honestly

Table 6: 2030 demand projections compared

| Forecaster | 2030 projection | Methodology bias |

| IEA base case | ~945 TWh global DC demand (~3% of global electricity) | Bottom-up from accelerator server shipments; conservative on speculative buildouts |

| Goldman Sachs | +160% DC power demand growth | Top-down, investment-led; treats power as the binding constraint on AI |

| Grid Strategies (US peak) | ~90 GW of data center-driven peak load growth in utility forecasts | Aggregates utility filings; inherits any utility over-forecasting |

| LBNL (US AI servers) | 165-326 TWh by 2028 | Narrow scope, hardware-based; most defensible floor estimate |

The IEA’s server-shipment methodology is the most disciplined, because chips that are never manufactured cannot consume power, and supply chains are observable. The utility-filing numbers are the least reliable as forecasts, because interconnection queues are full of duplicate and speculative requests; the same prospective data center often appears in multiple utilities’ pipelines. The truth for 2030 most likely lands between the IEA base case and Goldman’s scenario, with the deciding variable being how fast inference demand from agentic and video workloads compounds.

One constraint flip worth flagging: through 2024 the binding limit on AI buildout was GPU supply. By 2026, multiple operators have slowed cluster expansion because of power availability, not chip availability. Energy is now the gating resource, which is precisely why the nuclear deals in Table 5 exist.[Pew Research — what we know about US data center energy use]

What this means for enterprises and investors

Cloud pricing has a power floor. GPU instance pricing increasingly reflects electricity procurement costs and scarcity, not just silicon depreciation. Regions with constrained grids such as Northern Virginia and Dublin will carry persistent price premiums; expect cloud providers to steer AI workloads toward power-rich regions with pricing incentives.

Latency vs megawatts is the new siting trade-off. Facilities are moving to where power is, not where users are. For enterprises with data residency requirements, this collides directly with sovereignty rules, a dynamic covered in our South Asia data sovereignty analysis.

Power purchase visibility is now a vendor due-diligence question. If your AI roadmap depends on a provider scaling capacity 10x by 2028, that provider’s energy contracts matter as much as its model benchmarks. The hyperscalers’ nuclear PPAs are, among other things, an enterprise sales document.

The second-order trades. Data center REITs, grid equipment makers, liquid cooling suppliers, and uranium are all downstream of Table 3. Pakistan’s decision to allocate roughly 2,000 MW to bitcoin mining and AI data centers is the same global story playing out in a power-deficit country, covered in our Pakistan AI economy analysis. For how power constraints shape the chip market, see our Nvidia chip competition scorecard.

FAQ

How much electricity does an AI data center consume?

A typical AI-focused hyperscale facility uses as much electricity per year as roughly 100,000 households. The largest under construction will draw about 20 times more, with frontier campuses like Stargate and Colossus 2 targeting more than 1 gigawatt of continuous power, comparable to a large nuclear reactor’s output.

Why are AI companies buying nuclear power?

AI inference runs 24/7 at load factors above 80%, which renewables alone cannot serve without massive storage. Nuclear provides carbon-free baseload at 90%+ capacity factors. Microsoft, Amazon, Meta, and Google have collectively signed deals representing roughly 10 GW of current and future nuclear capacity since late 2024.

What is AI data center power density?

The electrical load per server rack. Legacy racks draw 5-15 kW; current Nvidia GB200 NVL72 racks draw 120-140 kW and require liquid cooling; next-generation Rubin-class systems are projected at 250-900 kW per rack by 2027.

Will AI data centers strain the US grid?

In specific regions, they already do. Data centers consume about 26% of Virginia’s electricity, and roughly 90 GW of forecast US peak load growth is tied to data centers. The national grid can absorb the growth; the five regional clusters where capacity concentrates are where the strain, and the rate increases, will show up first.

Is the demand forecast reliable?

Partially. Utility interconnection queues contain duplicate and speculative requests, and Georgia regulators’ own staff warned about over-forecasting before approving nearly 10 GW of new capacity. The IEA’s hardware-shipment-based projections are the most conservative credible floor.