US-China Tech War 2026: Who is Winning the AI Race?

The Brief

The Pulse US chip export policy toward China reversed direction twice in five months in 2026. On January 13, the Commerce Department’s Bureau of Industry and Security shifted its licensing posture for Nvidia H200 and AMD MI325X-class chips from presumption of denial to case-by-case review, codifying a loosening President Trump had announced the previous December. […]

Why It Matters

The story matters because it changes how buyers, builders, or policymakers should read the AI Policy and Power market.

Watch Next

Watch whether the signal becomes a budget, procurement, or platform decision in the next cycle.

The Pulse

US chip export policy toward China reversed direction twice in five months in 2026. On January 13, the Commerce Department’s Bureau of Industry and Security shifted its licensing posture for Nvidia H200 and AMD MI325X-class chips from presumption of denial to case-by-case review, codifying a loosening President Trump had announced the previous December.

On May 31, the same agency moved in the opposite direction, closing a loophole that had let China-headquartered firms acquire Nvidia’s most advanced Blackwell processors through subsidiaries located outside China.

That whiplash is not a sign of policy confusion so much as a genuine, unresolved tension inside US strategy: the same administration that wants to keep the most advanced AI compute out of Chinese hands for national security reasons also wants US chipmakers to keep selling into the world’s second-largest technology market before Chinese domestic alternatives mature enough to make American chips unnecessary.

Meanwhile, the AI model layer tells a less ambiguous story. Chinese labs, cut off from the most advanced chips for years, have closed the capability gap with US frontier models faster than most 2023-era forecasts assumed possible, doing it with lower training budgets and openly licensed weights spreading globally.

This scorecard covers both halves of that story, chips and models, using the most current, attributable figures available.

Core Significance

Why it matters:

- The May 31 guidance closed a loophole regulators believe had already moved a meaningful volume of restricted chips into Chinese hands indirectly: Industry sources cited by Reuters estimated that hundreds of thousands of advanced processors may have flowed to subsidiaries of Chinese AI firms based in third countries over roughly the prior year, suggesting the January-to-May policy loosening had a real, measurable effect on chip availability before the loophole closed. [Al Jazeera US says ban AI chip shipments applies Chinese firms outside China]

- Policy analysts have publicly questioned whether the current framework can achieve either of its stated goals simultaneously: The Council on Foreign Relations characterized the January 2026 rule as strategically incoherent, arguing that a large volume cap set high enough to preserve significant chip sales to China, while regulators estimated it could still supply enough processors for one of the largest AI data centers in the world, does not clearly serve either the national security objective or a coherent commercial one. [CFR new AI chip export policy China strategically incoherent unenforceable]

- The January 2026 rule replaced a Biden-era global tiering system with a more targeted, case-by-case licensing framework specifically for China-bound advanced chips: The Bureau of Industry and Security required exporters to certify specific technical, business, and end-user details, including identification of remote end users in named countries of concern, a structural shift from blanket country-tier restrictions toward transaction-level review. [Mayer Brown administration policies advanced AI chips codified]

Deep Context: How the Chip Policy Got Here, and Why the Model Gap Closed Anyway

The current back-and-forth traces to a reversal that began in December 2025, when President Trump announced the US would permit sales of previously banned Nvidia H200 and AMD MI325X-class chips to China, a departure from the Biden-era AI Diffusion Rule, which had blocked flagship GPU sales to China entirely while carving out lower-performance chips as an approved green zone. [Built In Trump lifted AI chip ban China clearing Nvidia AMD]

Approximately ten Chinese firms, including Alibaba, Tencent, and ByteDance, were cleared to purchase H200 chips under the new framework, each capped at 75,000 units. But as of the policy’s early implementation, no actual chip deliveries had been confirmed, with the arrangement caught in a mix of continued legal uncertainty and China’s own domestic supply chain regulations discouraging reliance on US hardware. Nvidia CEO Jensen Huang, who joined President Trump’s May 2026 state visit to China, publicly expressed hope for a breakthrough in the stalled sales even as the deal remained unresolved.

As covered in our Data Sovereignty report, export control policy increasingly functions as a proxy battlefield for a much broader argument about which country controls the physical infrastructure underneath AI, not just the software layer. The chip policy whiplash of 2026 is that argument playing out inside a single administration in real time, not just between the US and China.

Export Controls Constrained Chinese Labs, But the Response Was Efficiency, Not Stagnation

The Center for Strategic and International Studies has documented that years of hardware restrictions pushed Chinese AI labs toward aggressive software and architecture efficiency gains rather than halting their progress. CSIS’s analysis, citing evaluation work from the Center for AI Standards and Innovation, found the capability gap between DeepSeek’s V4 Pro model and the leading US models sits at roughly eight months, a dramatically narrower gap than existed even two years earlier. [CSIS what to know about Chinese AI models]

CSIS’s framing is notably measured: the analysis states plainly that Chinese models are now capable enough, cheap enough, and open enough to meaningfully shape global AI adoption, particularly where cost and open licensing matter more than absolute frontier capability, while also noting the US retains real, structural advantages in compute scale and closed-frontier model performance.

Data Insights

By the Numbers:

Figures in this section are drawn from Stanford HAI’s 2026 AI Index as cited in industry analysis, and from independent AI model benchmark trackers, with each figure attributed to its specific source given how quickly these numbers shift.

- Stanford HAI’s 2026 AI Index, as cited in industry analysis, put the benchmark performance gap between the best US and Chinese AI models at approximately 2.7 percentage points, down from a range of roughly 17.5 to 31.6 points measured in May 2023: The same analysis cited US private AI investment at approximately 285.9 billion dollars in 2025 against roughly 12.4 billion dollars for China, a large absolute gap in capital deployed that coexists with a rapidly narrowing capability gap, illustrating that spending scale and output capability are not moving in lockstep. [Digital in Asia China vs US 2026 comparison AI race]

- The Chinese open-weight AI field expanded from a single prominent lab to several credible, frontier-adjacent competitors within roughly eighteen months: Zhipu AI’s GLM-5.2, released June 13, 2026 under an MIT license with a 1 million token context window, joined DeepSeek, Alibaba’s Qwen line, and Moonshot AI’s Kimi as labs shipping openly licensed models that independent trackers rank competitively against Western systems on coding and agentic benchmarks specifically, with Zhipu itself going public in Hong Kong in January 2026. [GEO Toolbox Chinese AI models compared DeepSeek Qwen GLM Kimi]

- Independent, verified leaderboards rather than vendor-published marketing figures are increasingly the standard both Chinese and Western labs submit results to: That shift toward third-party verified benchmarking, rather than self-reported vendor claims, is itself a meaningful data point about how contested and commercially consequential benchmark credibility has become as the performance gap has narrowed.

Table 1: 2026 Chip Export Policy Timeline

| Date | Action | Direction | Chips affected | Status |

| December 8, 2025 | Trump announces policy change | Loosening | H200, MI325X-class | Announcement |

| January 13, 2026 | BIS final rule codifies change | Loosening | H200, MI325X-class | Case-by-case review replaces presumption of denial |

| May 2026 | Trump state visit to China, Huang attends | Neutral, diplomatic | H200 sales discussed | Deal remained unresolved |

| May 31, 2026 | BIS closes subsidiary loophole | Tightening | Blackwell, Rubin, MI350x-class | Applies to China-headquartered firms globally |

Table 2: Capability and Investment Gap, US Versus China

| Metric | Figure | Source |

| AI benchmark performance gap, 2026 | Approximately 2.7 percentage points | Stanford HAI 2026 AI Index, as cited |

| Same gap, May 2023 | Approximately 17.5 to 31.6 points | Stanford HAI 2026 AI Index, as cited |

| DeepSeek V4 Pro gap to leading US models | Approximately 8 months | CAISI evaluation, cited by CSIS |

| US private AI investment, 2025 | Approximately 285.9 billion dollars | Cited industry analysis of Stanford HAI data |

The Business Case: What the Policy Whiplash Means for Enterprise AI Procurement

For enterprises with global operations or supply chains touching China, the practical lesson from five months of reversing chip export policy is that compliance obligations tied to Chinese entities can change with a single weekend guidance update, as the May 31 subsidiary loophole closure demonstrated. Any enterprise routing AI infrastructure procurement through offshore subsidiaries or third-country entities connected to Chinese parent companies needs export control review built into procurement as a standing process, not a one-time check.

For enterprises evaluating AI model vendors, the capability and cost data tell a more actionable story than the chip policy does. Chinese open-weight models are increasingly viable options specifically for cost-sensitive, high-volume workloads where absolute frontier capability is not the deciding factor, though enterprises should weigh that option against the same data sovereignty and content moderation considerations that apply to any AI system whose training and operation sit outside a company’s home jurisdiction.

As covered in our Open Source AI Model Releases report, the broader 2026 pattern is that open-weight model leadership has shifted meaningfully toward Chinese labs at the same time a major Western lab, Meta, stepped back from frontier open releases. Enterprises building AI infrastructure strategy now need country-of-origin and licensing review as a standard part of open-weight model evaluation, not an afterthought.

Expert Nuance: Benchmark Credibility Itself Has Become a Contested Battleground

A pattern worth flagging for anyone reading benchmark comparisons between US and Chinese models is that methodology now matters as much as the headline score. Comparisons that rely on vendor-published marketing figures routinely produce different rankings than comparisons using independent, third-party leaderboards that verify submitted results, and the gap between those two methodologies has grown as the commercial and geopolitical stakes of benchmark leadership have risen. [TechJack Solutions Qwen vs DeepSeek 2026]

That methodological caution applies in both directions. Chinese labs have faced credible accusations, including from Anthropic in February 2026, of using fraudulent accounts to extract training data from Western models, a practice that would artificially inflate a Chinese model’s apparent capability gains if the accusation is accurate. Western labs have also faced periodic scrutiny over benchmark selection and reporting practices that favor their own models. Neither pattern invalidates the broader trend of a narrowing capability gap, but both are reasons to weight independently verified, multi-source benchmark data more heavily than any single vendor’s published claim, regardless of which country that vendor is based in.

The practical takeaway for procurement and technical teams is the same discipline that applies to any vendor evaluation: request the specific benchmark methodology, check whether results were independently verified, and treat any single benchmark score as one data point rather than a definitive capability ranking.

Strategic Outlook

- Watch whether the May 31 subsidiary loophole closure holds, or whether new workarounds emerge given the scale of chip volume industry sources say previously moved through it: With industry estimates suggesting hundreds of thousands of advanced processors may have already reached Chinese firms through offshore subsidiaries before the closure, enforcement effectiveness over the second half of 2026 will be a clearer signal of policy durability than the guidance itself.[US takes step halt Nvidia AI chip shipments Chinese firms outside China Reuters]

- Expect continued oscillation in chip export policy as the underlying tension between national security and commercial access remains unresolved: Nothing about the structural disagreement CFR identified in January, that the current framework cannot simultaneously maximize national security restriction and commercial chip sales, has been resolved by the May tightening, suggesting further policy adjustment in either direction remains likely rather than a settled equilibrium.

- Watch whether Chinese labs’ open-weight strategy continues gaining global adoption share specifically in markets outside the US and China: With CSIS noting that a cheaper, more open model can spread through developer ecosystems in ways a closed frontier model cannot, the more consequential long-term competition may be over global default adoption in Southeast Asia, Latin America, and Africa rather than over which country’s labs hold the absolute frontier benchmark lead at any given moment.

Key Question Answered

Who is winning the US-China AI competition in 2026?

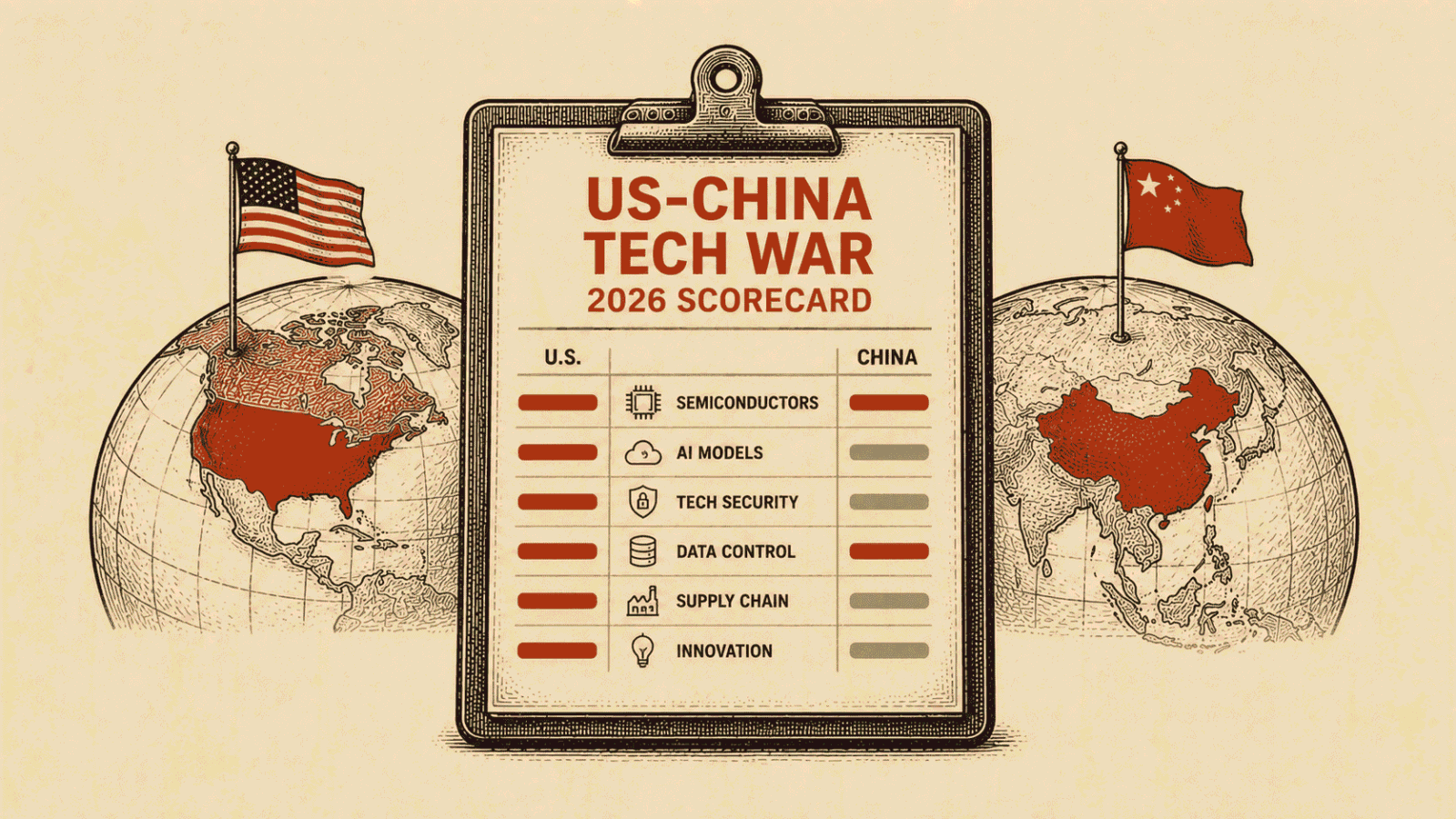

The honest answer depends entirely on which dimension is being measured, and the available data does not support a single, confident verdict. On chip export policy, the US retains substantial control over the most advanced compute, but that control has been applied inconsistently, loosened in January 2026 and tightened again in May, reflecting genuine, unresolved tension between national security and commercial goals rather than a settled strategy.

On AI model capability, Chinese labs have narrowed the benchmark gap with US frontier models to roughly 2.7 percentage points as of 2026 according to Stanford HAI data cited in industry analysis, down from double digits in 2023, while US private AI investment still outpaces China’s by a wide multiple.

On global adoption specifically, Chinese labs including DeepSeek, Qwen, and Zhipu AI’s GLM have built a meaningful lead in openly licensed model downloads, a distribution advantage that operates somewhat independently of who holds the frontier capability lead. The most defensible summary is that the US retains an edge in raw compute access and closed-frontier model capability, while China has built real strength in cost-efficient development and open-weight distribution, and neither advantage currently looks decisive or permanent.

The Takeaway

The US-China technology competition in 2026 resists the simple scoreboard framing that headlines often apply to it. Chip export policy reversed direction twice in five months, evidence of a strategy still being negotiated internally rather than a fixed doctrine. AI model capability gaps that looked wide and durable in 2023 have narrowed to single digits by 2026, achieved by Chinese labs operating under real hardware constraints rather than despite an absence of them.

Both halves of that story matter for anyone making infrastructure or vendor decisions in 2026, and neither can be safely ignored in favor of the other. Export control status can change with a single weekend guidance update, as the May 31 loophole closure demonstrated, making compliance a continuous process rather than a one-time check for any enterprise with China-adjacent supply chains. Model capability and licensing terms are shifting fast enough, and independently enough of chip policy, that vendor evaluation built around a fixed assumption about which country’s models are categorically better is already out of date.

For enterprises and policymakers alike, the more useful question for the remainder of 2026 is not which country is winning an undifferentiated tech war. It is which specific dimension, compute access, model capability, cost efficiency, or global distribution, actually matters most for a given decision, since the data shows clearly that the answer is not the same across all four.