The Rise of Edge AI: Why Enterprises are Moving AI Off the Cloud

The Brief

The Pulse The global edge AI market is on a trajectory to grow from roughly 24.9 billion dollars in 2025 to nearly 119 billion dollars by 2033, a 21.7% compound annual growth rate driven by three forces that have converged specifically in 2026: data sovereignty regulation, collapsing edge hardware costs, and the practical inadequacy of […]

Why It Matters

The story matters because it changes how buyers, builders, or policymakers should read the AI Infrastructure market.

Watch Next

Watch whether the signal becomes a budget, procurement, or platform decision in the next cycle.

The Pulse

The global edge AI market is on a trajectory to grow from roughly 24.9 billion dollars in 2025 to nearly 119 billion dollars by 2033, a 21.7% compound annual growth rate driven by three forces that have converged specifically in 2026: data sovereignty regulation, collapsing edge hardware costs, and the practical inadequacy of cloud-only AI for latency-sensitive enterprise workloads.

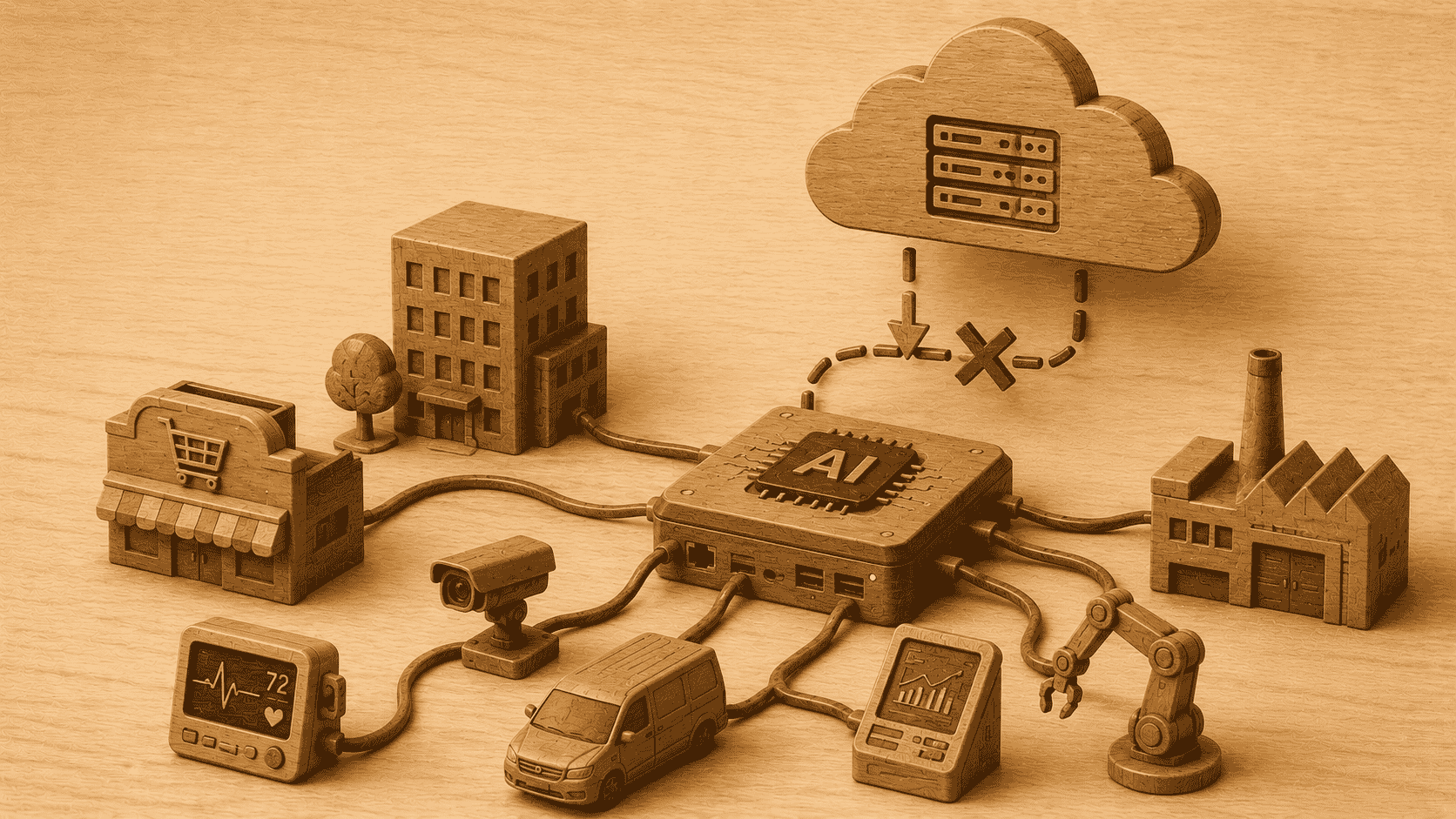

Edge AI describes AI inference that runs at or near the source of data rather than in a centralized cloud. The inference happens on the factory floor, in the hospital room, inside the vehicle, or on the enterprise campus, not in a data center hundreds of miles away.

For enterprises paying for cloud inference at scale, the economics case alone is becoming compelling. Enterprises spent approximately 40 billion dollars on cloud AI inference in 2024, paying for every API call, every image processed, and every voice command routed to a remote data center. Moving that inference to the edge cuts the per-query cost, reduces latency to milliseconds, and keeps sensitive data inside the organization’s own infrastructure.

Core Significance

Why it matters:

- Manufacturing is the fastest-growing edge AI vertical, projected at a 23% CAGR through 2033: The hardware segment currently leads the edge AI market with over 51% of revenue share, concentrated in the specialized processors, edge gateways, and AI accelerators that run inference at the factory floor rather than routing production data off-site. [Grand View Research edge AI market size forecast 2026 2033]

- Neural Processing Units are replacing GPUs at the edge because they consume 10 to 20 times less power for the same inference output: Major chip manufacturers including Intel and AMD are now embedding NPUs directly into industrial-grade hardware, meaning edge deployments running predictive maintenance or vision inspection systems can justify the investment through energy savings alone within 18 months. [TechAhead edge AI manufacturing enterprise trends 2026]

- Data sovereignty regulation is converting edge AI from a performance choice into a compliance requirement: The EU Data Act, enforceable since September 2025, bans data lock-in clauses and effectively requires that personal and industrial data from European operations stay within member-state borders, a mandate that is forcing cloud-dependent architectures to add local processing layers regardless of whether enterprise IT teams prefer it. [Mordor Intelligence edge computing market 2026 2031]

ISO 27001 auditors now expect proof of local log retention as part of standard certification requirements, tying compliance directly to edge infrastructure deployment in a way that was not consistently enforced two years ago.

Deep Context: Why cloud-first AI hits a ceiling in real enterprise operations

The cloud-first AI narrative assumes that latency is a minor inconvenience and bandwidth is cheap. In production manufacturing, autonomous vehicles, real-time clinical diagnostics, and industrial automation, neither assumption holds.

BT Group and AWS Wavelength demonstrated in 2024 that dedicated edge AI service deployments can cut data latency by 40% compared to standard cloud routing. Bosch integrated edge AI modules into its smart factories in 2024 and achieved a 30% reduction in machine downtime through on-site predictive maintenance that does not require sending sensor data to a remote cloud for analysis. [SkyQuestTT edge AI market size trends forecast 2026 2033]

As covered in our training vs inference report, inference now accounts for 80 to 90% of AI’s total compute and electricity cost over the lifetime of a deployed system. Moving inference to the edge does not eliminate that cost, but it shifts it from a per-query cloud API charge that scales with usage to a fixed hardware and energy cost that stays roughly flat regardless of query volume.

The hardware buildout is already underway at major enterprise vendors

In March 2026, Dell Technologies announced advancements in its enterprise edge infrastructure portfolio specifically designed to support AI workloads and distributed computing environments, with a focus on operational resilience and real-time analytics closer to data sources.[MarketsandMarkets edge computing market size share forecast]

Qualcomm announced a partnership with IBM in March 2025 to ship IBM Granite 3.1 models on Qualcomm’s AI Hub and Cloud AI accelerators, enabling efficient low-power generative AI inference on Snapdragon devices at the edge with IBM Watson governance policy controls layered on top. Google and Synaptics announced a parallel collaboration to integrate Google’s MLIR-compliant ML core into Astra AI-Native hardware for on-device multimodal edge AI.

Data Insights

By the numbers:

All figures from named market research firms and industry analysts cited inline.

- The edge AI market grew 29% year over year from 2025 to 2026, from 29.08 billion dollars to 37.51 billion dollars: That single-year growth rate outpaces most adjacent technology markets and reflects accelerating real enterprise deployments beyond the pilot phase that characterized 2023 and 2024. [Research and Markets edge AI market report 2026]

- The broader edge computing market reached 257.76 billion dollars in 2026 on a trajectory to 479.97 billion by 2031: At a 13.24% compound annual growth rate, the market is expanding as enterprises deploy edge infrastructure for AI-enabled workloads, real-time monitoring, and localized analytics, driven by 5G rollouts, IoT deployments, and data sovereignty requirements acting simultaneously.

- Edge AI chip design is diversifying away from GPU dependency in 2026: Custom AI chips from cloud providers and semiconductor firms are enabling efficient edge inference that reduces reliance on centralized GPUs, with the transition from experimental deployments to large-scale commercial rollout accelerating specifically in industrial and healthcare applications. [DataM Intelligence edge AI market growth industry forecast]

As covered in our AI data center power consumption pillar, the same power density challenges pushing data centers toward liquid cooling at the infrastructure level are pushing enterprises toward edge deployments where NPU-equipped devices can handle inference workloads at a fraction of the power draw of a GPU-based cloud query.

Table 1: Edge AI deployment by vertical and primary driver

| Vertical | Deployment stage | Primary driver | Key metric | 2026 CAGR outlook |

| Manufacturing | Full commercial rollout | Real-time defect detection, predictive maintenance | Downtime reduction, 18-month hardware ROI | 23% through 2033 |

| Healthcare and life sciences | Accelerating | Real-time diagnostics, remote patient monitoring | Compliance, HIPAA, point-of-care accuracy | Fastest growing segment |

| Automotive and autonomous | Pilot to commercial | Sub-10ms latency for safety decisions | Latency, reliability, regulatory approval | 14.11% CAGR |

| Financial services | Early deployment | GDPR, data sovereignty, fraud detection latency | Regulatory compliance, detection speed | Emerging |

| Government and smart cities | Growing | Public safety, traffic, real-time services | Response time, local data control | Significant 2025 market share |

Table 2: Cloud AI inference versus edge AI inference compared

| Dimension | Cloud AI inference | Edge AI inference |

| Latency | Tens to hundreds of milliseconds | Single-digit milliseconds |

| Cost model | Per-query variable, scales with usage | Fixed hardware plus energy, flat at scale |

| Data sovereignty | Data leaves the facility | Data stays on-premises |

| Connectivity dependency | Requires reliable broadband | Functions offline or on degraded connectivity |

| Hardware requirement | Minimal at client, all compute in cloud | NPU or GPU at edge device, 10 to 20x more efficient per inference |

The Business Case: When edge AI makes financial sense over cloud

The financial case for edge AI is strongest when three conditions align: query volume is high and predictable enough to make fixed hardware costs competitive with variable API pricing, latency below 10 milliseconds is operationally necessary rather than just preferable, and the data being processed carries regulatory or contractual sensitivity that adds real risk to cloud routing.

Manufacturing at scale is the cleanest illustration. A production line running vision inspection at 1,000 items per minute generates millions of inference queries daily. At cloud API pricing, that volume produces a significant ongoing cost that grows with throughput. At edge pricing, the same workload runs on deployed hardware with energy costs that stay roughly constant regardless of whether throughput increases 50%.

Organizations that do not meet all three conditions are not necessarily wrong to stay cloud-first for AI inference. The edge case weakens significantly for low-volume workloads, for applications where sub-100ms latency is adequate, and for organizations that lack the internal engineering capacity to manage distributed edge infrastructure. Hybrid deployments, where the edge handles real-time inference and the cloud handles long-term analytics and model updates, are increasingly the dominant enterprise architecture rather than a pure choice between one and the other.

Expert Nuance: The regulatory mandate is doing more work than most market analysis acknowledges

Market research projections for edge AI typically lead with performance and cost as the primary demand drivers. The faster-accelerating demand driver in 2026 is regulatory compliance, specifically the EU Data Act and equivalent statutes in Saudi Arabia and India that replicate similar local-data-retention requirements.[Precedence Research edge AI market attain 165 billion 2035]

The practical consequence is that enterprises with European, Saudi, or Indian operations face an infrastructure mandate that makes cloud-only AI architectures legally problematic regardless of whether the performance case is compelling. ISO 27001 auditors expecting proof of local log retention are effectively requiring edge infrastructure as a prerequisite for certification renewal.

This regulatory channel has produced a category of enterprise edge AI deployments that are not primarily technology decisions. They are compliance decisions that happen to require AI-capable edge hardware, which is a materially different purchase dynamic than one driven by performance benchmarks alone, and it means demand is less sensitive to cloud API price reductions than the performance-driven market analysis typically assumes.

Strategic Outlook

- Watch the EU Data Act’s first major enforcement actions as the signal that regulatory edge demand is locked in: The Act became enforceable in September 2025. Its first significant enforcement actions, expected in 2026 to 2027, will either validate the compliance-driven edge demand thesis or reveal that enforcement is less aggressive than the legislation suggested, which would change the pace of mandated deployments.

- Early enterprise movers in edge AI are building compounding advantages that compound faster than the market realizes: Organizations that deploy edge AI infrastructure now are accumulating institutional knowledge in edge deployment, optimizing models for on-device constraints, and building hardware partnerships that later entrants will pay a premium to replicate.[Medium Vygha edge AI dominance 2026 80 percent inference locally]

- The custom silicon shift means edge AI hardware is becoming a strategic procurement decision, not a commodity: As cloud providers and chip companies design inference silicon specifically optimized for edge workloads, the choice of edge hardware in 2026 increasingly determines which AI software ecosystem an enterprise is compatible with three to five years later, creating a lock-in dynamic that mirrors the GPU-to-CUDA dependency story at the data center level.

Key Question Answered

Why are enterprises moving AI inference to the edge in 2026?

Three forces are converging. First, edge hardware costs have dropped to the point where Neural Processing Units, which consume 10 to 20 times less power than equivalent GPU inference, deliver returns within 18 months for high-volume enterprise workloads. Second, the EU Data Act, enforceable since September 2025, plus equivalent legislation in Saudi Arabia and India, effectively mandates local data processing for regulated operations regardless of performance preferences. Third, production applications requiring sub-10 millisecond response times, vision inspection, autonomous vehicle safety systems, real-time clinical diagnostics, cannot function reliably over cloud architectures where round-trip latency typically runs between tens and hundreds of milliseconds.

The edge AI market growing at 29% year over year in 2026 and at a projected 21.7% CAGR through 2033 reflects all three drivers simultaneously. Cloud AI remains the right architecture for low-volume, latency-tolerant, low-sensitivity workloads. Edge AI is becoming the mandatory architecture for everything else.

The Takeaway

The cloud-first AI narrative was always a simplification. It worked as a default for most enterprise workloads during 2022 and 2023 because most enterprise AI deployments were low-volume, experimental, and primarily text-based, exactly the conditions where cloud economics are favorable and latency rarely matters.

2026 is the year that narrative breaks at scale. Manufacturing at thousands of queries per second, hospital diagnostics at the point of care, autonomous systems making safety decisions in real time, none of those use cases fit the cloud-first assumption, and regulatory mandates in three major jurisdictions have now made the data sovereignty case independently of any performance argument.

The practical message for enterprise infrastructure leaders is that edge AI is no longer an emerging technology to evaluate on a roadmap. It is an active procurement decision that sits at the intersection of hardware costs, regulatory requirements, and AI software compatibility, and the organizations locking in edge infrastructure partnerships in 2026 are setting architectural constraints that will define their AI deployment flexibility for the next decade.